Introduction

The UK Emissions Trading Scheme (UK ETS) expands to maritime starting 1 July 2026. This article summarizes the scheme's scope and compliance mechanics as they apply to shipping, alongside how UK ETS modifiers and carbon pricing are intended to be handled in the Carbon Calculator. Like EU ETS, UK ETS percentages apply to the Carbon Cost calculation per voyage leg, determined by the relevant ports.

This feature requires the configuration flag CFGEnableUkEts to be enabled.

UK ETS Scope

From 1 July 2026, the UK ETS applies to cargo and passenger vessels of 5,000 GT and above. Offshore ships are brought into scope later, from 1 January 2027. The scheme covers emissions on domestic voyages between UK ports and emissions generated while in UK ports of call.

Phase-in and Reporting Timeline

Unlike EU ETS, which phases in surrender obligations over several years, the UK ETS applies a 100% surrender obligation from the start, but the first scheme year is a half-year.

|

Period |

Notes |

|---|---|

|

1 Jul – 31 Dec 2026 |

First (partial) scheme year; reporting begins 1 July |

|

2027 onward |

Standard reporting year, 1 Jan – 31 Dec |

Greenhouse Gases Covered

The greenhouse gases covered align with EU ETS and include combustion and slippage emissions of:

-

Carbon dioxide (CO₂)

-

Methane (CH₄)

-

Nitrous oxide (N₂O)

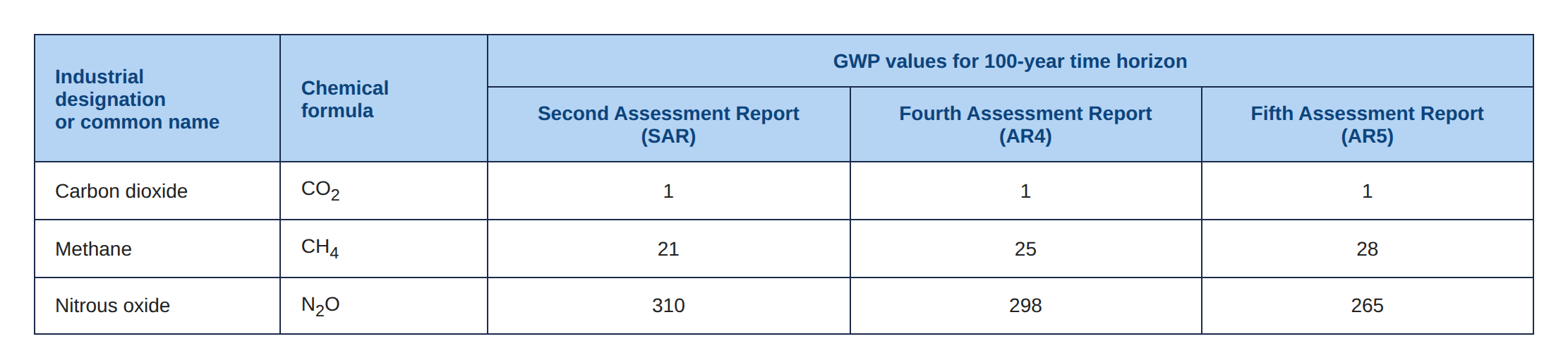

Emissions are calculated on a tank-to-wake basis. Methane and nitrous oxide are reported using IPCC AR5 global warming potential values: CH₄ = 28 and N₂O = 265. (Note: this is the same GWP convention used for EU ETS and differs FuelEU - AR4)

Domestic Voyages and Ports of Call

A domestic voyage includes any voyage from one UK port to another, as well as a voyage that starts and ends at the same UK port. This regulation covers 100% of domestic voyage emissions.

100% of Emissions generated during ports of call are also in scope, including time at berth, whether moored or anchored, at UK ports and offshore installations.

Because 100% of port-of-call emissions are captured, the port stay portion of an international route calling at a UK port is also within scope, even though the international voyage leg itself is not a domestic voyage.

Northern Ireland <–> Great Britain Deduction

A 50% deduction applies to the surrender obligation for voyages between Northern Ireland and Great Britain. Port stays in both Northern Ireland and Great Britain remain subject to a 100% surrender obligation.

For comparison, on a voyage between a non-UK port (e.g. France) and Great Britain, the voyage leg carries no (0%) surrender obligation, while the Great Britain port stay remains at 100%.

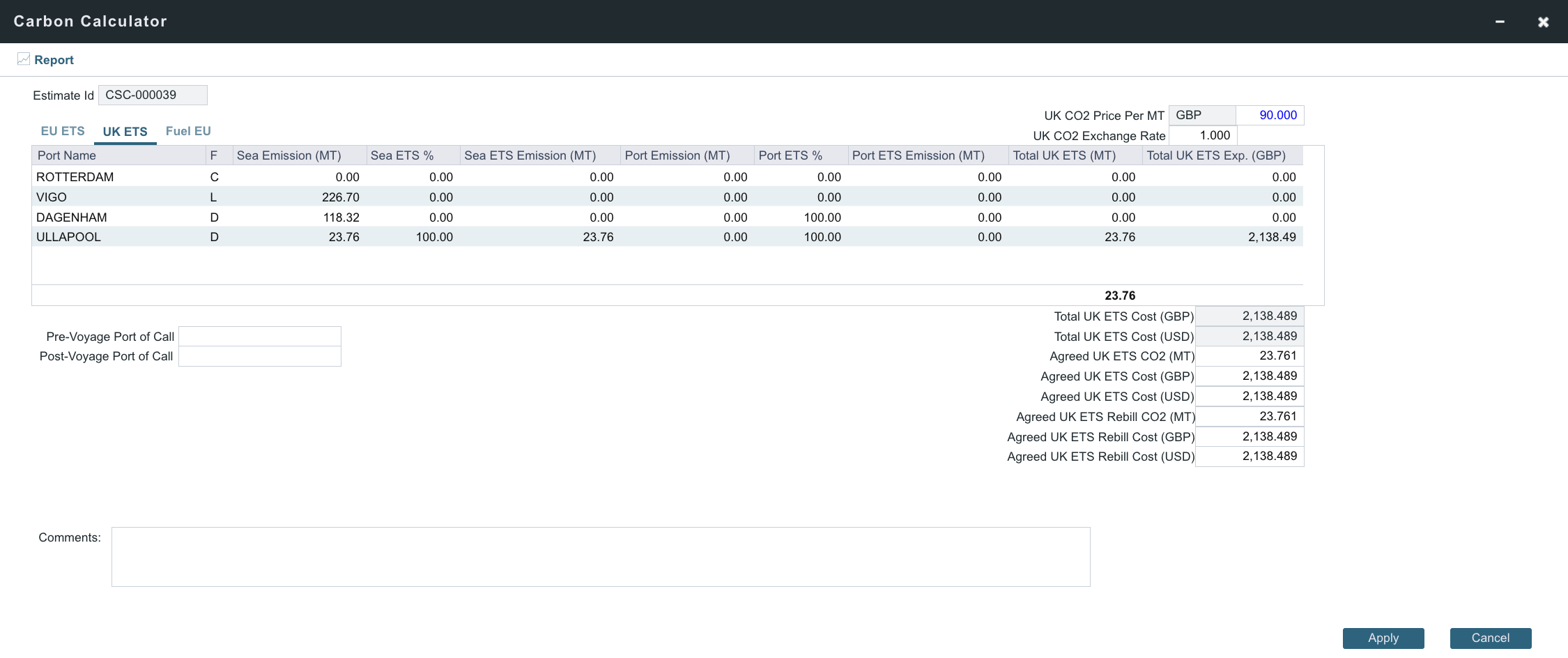

UK ETS in the Carbon Calculator

This feature requires the configuration flags CFGEnableUkEts and CFGDefaultIncludeUKETSExpInPnl to be enabled. Schema version 53.4 is also a requirement.

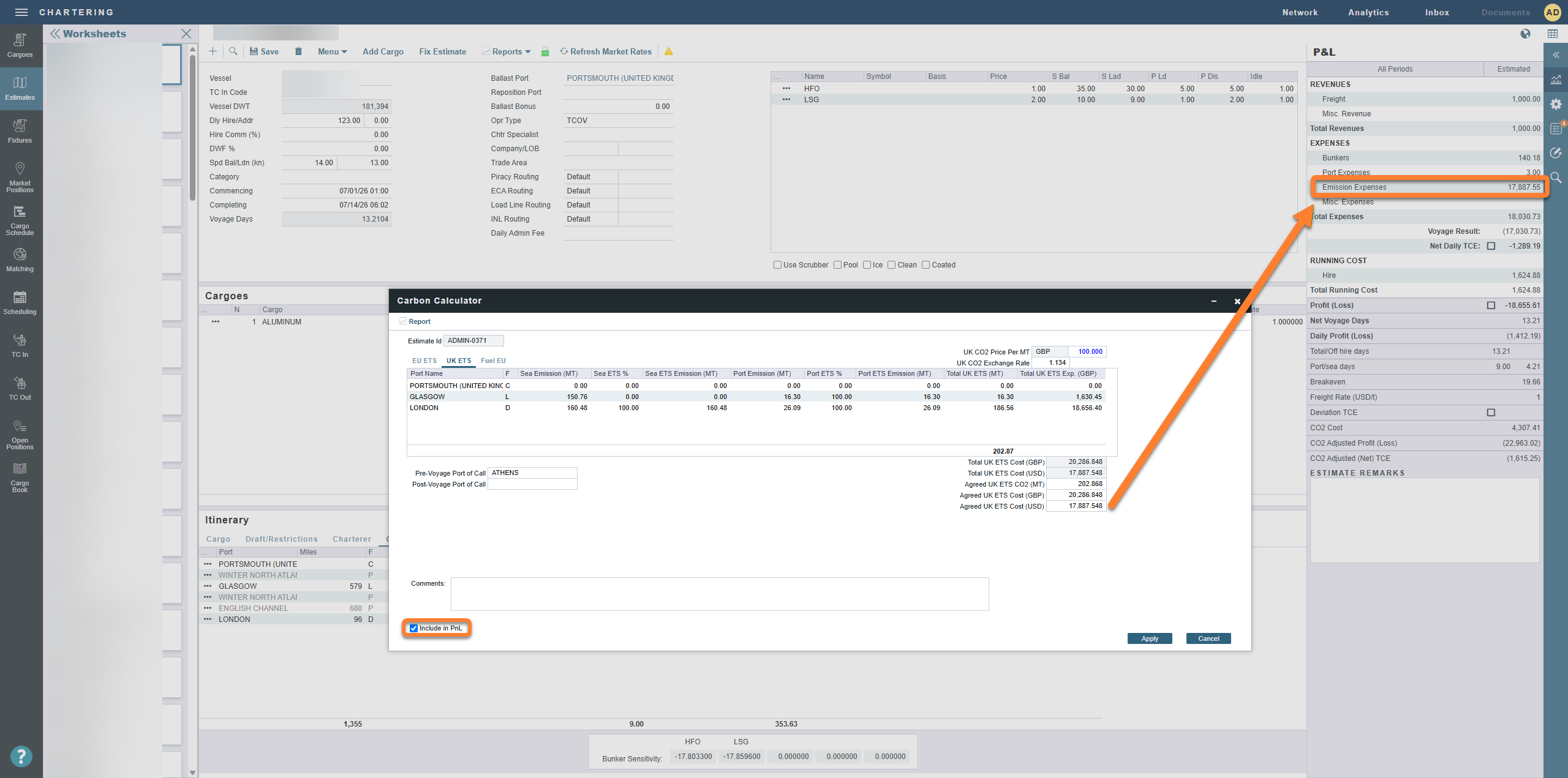

The UK ETS Calculator is available in the Carbon Calculator on the Estimate and Voyage level to aid in commercial decision-making regarding the impact of UK ETS, and to apply a price to carbon emissions. The percentage values for each leg of an itinerary will apply to the Carbon Cost calculation by default and will be determined by the Load and Discharge ports. You can also view the total UK ETS emissions in MT.

Select the Include in PnL checkbox to add UK ETS costs to the Estimate PnL or Voyage PnL.

Note: adding UK ETS costs to the PnL requires both selecting the Include in PnL checkbox and a settlement type for a contract.

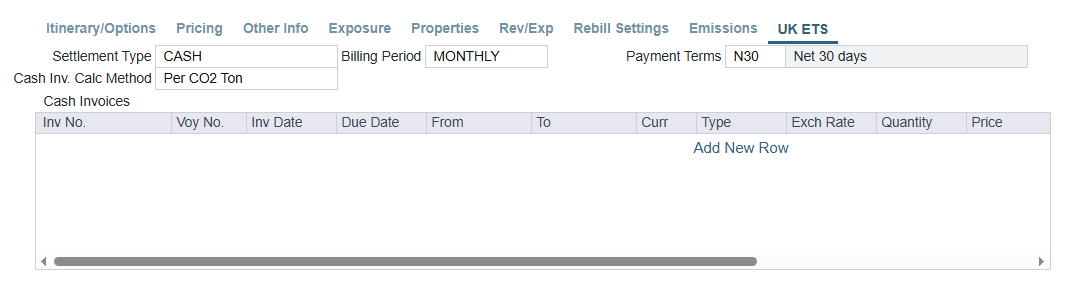

Contract Settlement Type Options

UK ETS expense allocation to a contract requires the configuration flag CFGEnableUKETSAllocation to be enabled and schema version 54.0. The UK ETS tab requires CFGEnableTCEmissionsAllocation for TC contracts and CFGEnableCargoEmissionsAllocation for Cargo and VC In contracts.

The settlement type Cash is available for selection on the UK ETS tab of the Cargo, VC In, Time Charter, or Head Fixture contract added to the Estimate. Selecting this option allows companies to allocate UK ETS expenses to a specific contract and the creation of cash invoices.

Business Rules Setup for UK ETS

See the Carbon Emissions Business Rules page for the specific Business Rules setup requirements for UK ETS financial workflows.

Fuel Type Setup for UK ETS

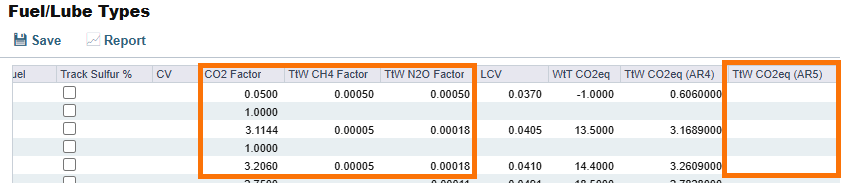

On the Fuel/Lube Types form, add TtW Co2eq (AR5) values for each fuel type.

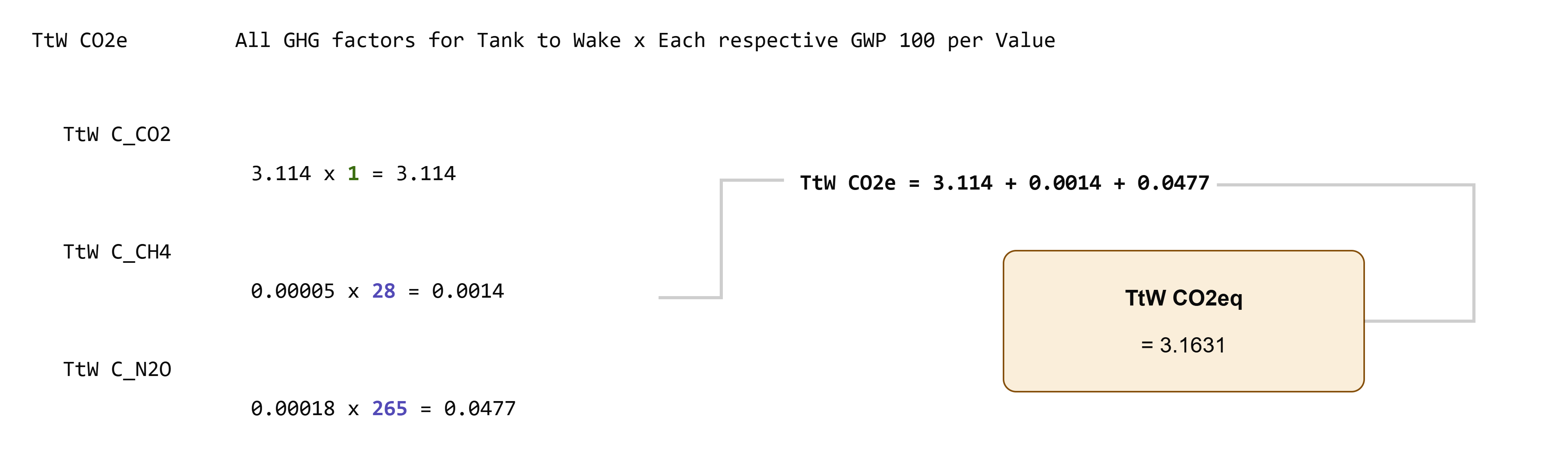

You can calculate AR5 values by multiplying the carbon dioxide (CO₂) factor, methane (CH₄) factor, and nitrous oxide (N₂O) factor fields by the AR5 assessment value for each fuel type.

Key factor fields in Fuel/Lube Types screen:

Example R5 calculation:

IPCC AR5 global warming potential values: CH₄ = 28, N₂O = 265, C0₂ = 1.

-

For clients without AR5 values, the system has a fallback method, and will use AR4 values. If AR4 values are missing, the system uses CO2 factors for calculations (AR5 → AR4 → CO2 factor)

-

TtW Co2eq (AR5) fields are also available in the Bunker Grades screen and bunker lifting level emissions.

Coming Soon: Creating cash/allowance invoices, accruals, reporting, and other financial workflows.